The Bank of Canada is responsible for setting the key interest rate in Canada, known as the overnight rate. When the Bank of Canada increases this rate rapidly, it can have several ramifications on the economy.

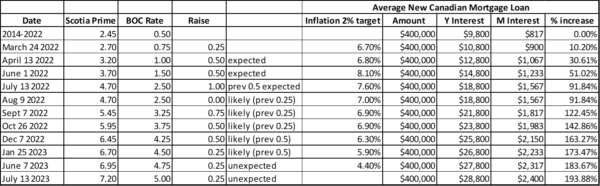

A significant increase from 0.50% to 5.00% in just 16 months represents a substantial tightening of monetary policy by the Bank of Canada. Such a rapid and substantial rate hike suggests a concerted effort to control inflation or address concerns about an overheating economy.

A rate increase of this magnitude over a relatively short period of time can have several implications which we will discuss.

There is no previous precedent of a 10-fold increase in the Bank of Canada’s interest rate occurring within just over one year. Such a dramatic and rapid increase would be unprecedented in the context of the Bank of Canada’s historical actions.

Historically, the Bank of Canada has typically implemented interest rate changes gradually and incrementally, taking into account various economic factors and indicators. Sharp and drastic rate increases could have significant consequences for the economy, including higher borrowing costs, impacts on the housing market, economic slowdown, exchange rate effects, debt servicing pressures, and market volatility.

The Bank of Canada (BoC) adjusts its overnight interest rate target based on its assessment of the economic conditions and its monetary policy goals. The magnitude and frequency of rate changes can vary depending on economic circumstances. Historically, the BoC has made gradual adjustments to the overnight rate rather than large, sudden changes. However, the specific changes per year can vary significantly.

To provide a general idea, in recent years, the Bank of Canada has typically made smaller adjustments to the overnight rate, ranging from 0.25% to 0.50% per change. For example, between 2015 and 2020, the overnight rate went from 0.50% to 1.75%, with several smaller increases and decreases during that period.

- From 2004 to 2007, the overnight rate increased from 2.50% to 4.50%, with several incremental hikes during that period.

- During the global financial crisis in 2008, the Bank of Canada implemented a series of significant rate cuts. The overnight rate decreased from 4.50% in December 2007 to 0.25% by April 2009.

- Following the recession, the Bank of Canada gradually increased the overnight rate from 0.25% in 2010 to 1.00% in 2011.

- From 2011 to 2014, the Bank of Canada maintained the overnight rate at 1.00% to support economic recovery and stability.

Here are some historical consequences of fast rate increases:

- Impact on borrowing costs: A rapid increase in the Bank of Canada’s interest rate leads to higher borrowing costs for businesses and consumers. This affects various types of loans, such as mortgages, business loans, and personal loans. As interest rates rise, borrowing becomes more expensive, which can discourage borrowing and investment.

- Cooling effect on the housing market: Higher interest rates make mortgages more expensive, which reduces affordability for potential homebuyers. As a result, demand for homes may decrease, leading to a slowdown or decline in the housing market. This can impact construction, real estate, and related industries.

- Economic slowdown: When the central bank increases interest rates rapidly, it aims to curb inflation and prevent the economy from overheating. However, if the rate hikes are too aggressive, it can lead to an economic slowdown. Higher borrowing costs reduce consumer spending and business investment, which can dampen overall economic activity.

- Exchange rate impact: A significant increase in interest rates can attract foreign investors seeking higher returns on their investments. This increased demand for Canadian currency can strengthen the exchange rate. While this may benefit imports and lower inflationary pressures, it can also make Canadian exports more expensive, potentially impacting trade and the competitiveness of export-oriented industries.

- Impact on debt servicing: Higher interest rates increase the cost of servicing existing debt for individuals, businesses, and governments. This can put pressure on highly leveraged entities, potentially leading to higher default rates and financial stress in the system.

- Stock market and investor sentiment: Rapid rate increases can trigger volatility in financial markets, particularly in bond and equity markets. As interest rates rise, the present value of future cash flows from stocks can be negatively affected, which can lead to a decline in stock prices. Investors may also become cautious or risk-averse, which can further impact market sentiment.

For a typical Canadian family, a rapid increase in interest rates can have various consequences. First, it leads to higher borrowing costs, particularly for families with variable rate mortgages. This means their monthly mortgage payments could increase significantly, leaving them with less disposable income for other expenses or savings. Additionally, higher mortgage rates reduce affordability, making it more challenging for families to enter the housing market or upgrade to a larger home. They may need to adjust their expectations, opt for a smaller property, or even delay their home purchase plans.

Furthermore, an economic slowdown resulting from rate increases can impact job security and wage growth for family members. This may result in reduced job opportunities, salary freezes, or even job losses. Such developments can have a significant impact on a family’s overall financial stability and ability to meet their financial goals.

In terms of exchange rate impact, if higher interest rates lead to a stronger Canadian dollar, it can affect the cost of imported goods and services. This means that prices for imported products such as electronics, clothing, or vehicles could rise, thereby affecting a family’s purchasing power and potentially leading to adjustments in their spending habits.

Moreover, higher interest rates increase the cost of servicing existing debt, such as credit card debt, personal loans, or student loans. Families may need to allocate more of their income towards debt repayment, which could limit their ability to save for emergencies or invest for the future.

Lastly, volatility in financial markets resulting from rate increases can impact investment portfolios, including retirement savings. If stock prices decline due to rising interest rates, the value of family investments or retirement funds may decrease. This may necessitate a reassessment of investment strategies or potentially lead to a delay in retirement plans.

It’s important to note that the specific impact on a typical Canadian family will depend on their unique financial circumstances, including income levels, debt levels, and the extent of their investments. Consulting with a financial advisor can provide personalized guidance to help navigate and mitigate potential challenges resulting from these factors.